Real estate is often called an “alternative” investment. That means it is an alternative to investments in stocks and bonds. Why is it good to have an alternative investment? The answer has to do with risk, reward, and a statistic called beta (β). In this article, we will define beta and explore why it is important to your investment strategy. We will also see how to look up and interpret a REIT’s beta statistic.

Risk and Reward

A good place to begin is with a simplified look at portfolio theory. The riskiness of your investment portfolio is directly related to the degree to which it is concentrated or diversified. There are two aspects of investment risk:

Along Comes Beta

Beta helps you to decouple individual returns from those of the overall market. It is a statistic that shows how well the returns of a particular asset track those of a particular market. It also indicates how volatile the asset is. Since REITs are stocks, their beta values relate to the stock market, usually represented by the S&P 500.

Market beta is, by definition, equal to 1.0 (or 100%). That means the following:

- An investment with a beta of 1.0 would owe all its returns to the movement of the market it measures against. That means the investment’s return may be equally volatile with those of the market and/or that those returns are highly correlated. Adding an investment with a beta of 1.0 to a well-diversified portfolio should not affect the portfolio’s risk.

- A beta greater than 1.0 could indicate an investment that moves with the market and/or is more volatile than the market. Adding an investment with a beta greater than 1.0 to a well-diversified portfolio should increase the portfolio’s risk.

- A beta of less than 1.0 indicates that only some of its returns are due to overall market movements. Adding an investment with a beta less than 1.0 to a well-diversified portfolio should reduce the portfolio’s risk.

- A beta of zero means that an investment’s returns are independent of market returns.

- A beta of -1.0 implies a 100% negative correlation between the investment and the market (e.g. a short position in a stock).

If you know an investment’s beta, you know how much of the investment’s return is due to market movement versus investment performance, i.e. systematic vs unsystematic risk.

Another way of thinking about β is relative risk: an investment with a β of 1.0 should be no riskier than overall market risk. We would say that this investment has no diversifiable risk, in that all its performance is explained by market performance. That is why adding the investment to a well-diversified portfolio adds no benefits of diversification to that portfolio – the portfolio’s risks and rewards remain the same. It is the task of a good investor to seek superior returns relative to investment risk.

When dealing with REITs, interpreting beta can be tricky. That is because REIT returns are not highly correlated with those of the stock market. Beta has the most meaning when the investment is highly correlated with the market to which it is compared.

Modern Portfolio Theory

No discussion of investment risks and rewards would be complete without including Modern Portfolio Theory, or MPT. MPT suggests that you can optimize the overall risk and return of your portfolio by making investments with a wide array of betas. Why? Because, when investments are decoupled, one can zig when the other zags. That is, when you add an investment with a beta less than 1.0 to your portfolio, your overall volatility of returns will decrease.

Now, so far, we’ve couched this discussion of beta in terms of picking stocks. But it is often used when referencing different markets and sectors. Returns on real estate investments are only weakly correlated to stock market returns. REITs usually have a beta lower than 1.0, and therefore reduce your portfolio’s volatility. This is the power of diversification writ large across different markets. If you want to reduce risks without necessarily lowering returns, you will seek out investments with a low, or even negative, beta. MPT tells us that this will not lower your overall returns, thereby helping to preserve your wealth.

Sometimes, REITs and REIT sector returns can have a beta greater than 1.0, even though REIT returns are not highly correlated with those of the stock market. Therefore, a REIT beta greater than 1.0 tells you that the investment is more volatile than the overall market.

REIT beta has more meaning when measured against the universe of REITs rather than the universe of stocks. If this beta figure were available, it would show you how well the returns of the REIT mirror those of the REIT universe.

The Betas of REITs

REITs deserve to be a significant part of your investment portfolio due to their excellent returns over time: 9.94% over the last 25 years, compared to 9.65% for the Russell 3000 index of stocks. But another reason to consider REITs is that most have relatively low betas. When you diversify your investments to include REITs, you are tying a part of your portfolio returns to the real estate market cycle, which typically averages 18 years. As you can probably guess, the real estate cycle drives REIT returns on a different timeframe from the business cycle (averages about four years) that influences stock returns. In other words, REITs might zig when stocks zag.

In fact, the long-term beta of the REIT market compared to the broad stock market (as measured by the S&P 500) is just 0.75. That beta is relatively low, considering both REITs and stock deliver strong long-term returns, and the REITs actually trade on the stock exchanges.

REIT Investment Strategies

We will mention two broad REIT investment strategies—holding and timing—to take advantage of the low beta between REITs and stocks.

Holding Strategy

In this strategy, you want to hold the broadest collection of REITs for the long-term, without trying to pick or time individual winners. You can accomplish this with a REIT exchange-traded fund (ETF) or a REIT mutual fund. With this strategy, you buy an index of REITs and hold it for the long term. This provides several advantages:

. With this strategy, you buy an index of REITs and hold it for the long term. This provides several advantages:

- You are broadly diversified, thereby minimizing unsystematic risk.

- Indexes are passively managed, meaning that your management fees are extremely low.

- You avoid trading commissions.

- You do not have to spend time researching individual REITs or predicting when the real estate market will enter a weak phase.

Disadvantages include:

- You must have the intestinal fortitude to ride out real estate bear markets without selling your REIT investments, knowing that in the long run, they will recover.

- You will not take advantage of any specialized knowledge that would lead you to think that you can profitably pick when to buy and sell individual REIT sectors and REITs.

Timing Strategy

You might want to time your purchase and sale of individual REITs and/or REIT sectors. This can provide advantages that include:

- Possibly beating the REIT market averages.

- Attempting to avoid real estate bear markets.

It requires skill (and luck) to consistently outperform an asset index.

Disadvantages include:

- Higher trading costs.

- Higher demand on your time and resources to make your selections.

- Possibility of making poor choices that hurt your overall performance.

- Possibility of being out of a bear REIT market when it turns around.

- You are less diversified when you are out of the market, thereby reducing the benefit of the weak beta between REITs and stocks.

- Your selections might have betas greater than 1.0 that increase your overall portfolio risk.

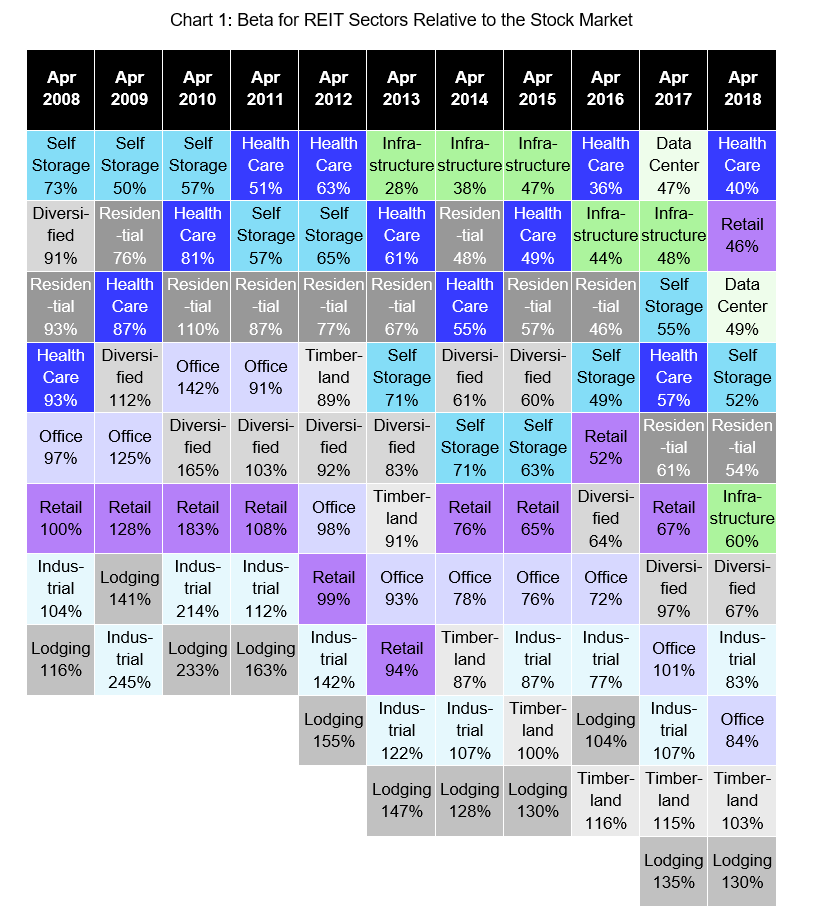

Nonetheless, if you want to try your hand at market timing, you should know the betas of individual REITs and REIT sectors so that you understand your overall risk exposure. The following NAREIT chart provides a summary of REIT sector betas over the last decade:

As you can see, while the overall long-term REIT beta is 0.75 (75%), some sectors in some years had betas greater than 1.0 (100%), thereby introducing additional risk to your portfolio. If you are extraordinarily skilled, that extra risk translates into higher than average returns. The converse is also true if you pick a loser.

You can find a REIT’s or REIT ETF’s beta listed in various financial sources, such as Yahoo. For example, you can find the beta for CT REIT here. We are not aware of any published source for current betas by REIT sector.

Conclusion

Beta measures how much of a security’s or sector’s performance is due to the general market. A beta below 1.0 indicates less correlation with the overall market and hence less risk. Studies show that REITs deliver a long-term beta of about 0.75, meaning you reduce your overall portfolio risk by adding in REITs to your investment mix.

This article is intended purely as educational content and should not be considered professional investment advice.

Nerd Corner

Beta

If you’re a math nerd, you’ll be interested to know that beta is calculated by dividing the covariance of an investment’s return by the variance of a portfolio or market return:

βi = Cov (ri, rm) / Var(rm)

where i = an investment, m = market portfolio, and r = return.

CAPM

The Capital Asset Pricing Model (CAPM) uses beta to predict the price of an investment within a given market. It takes the form of:

Ri = Rf + βi(Rm-Rf)

where Ri is the return on investment i, Rf is the risk-free rate of return, and Rm is the market return. Using CAPM, you can get an indication of the return you should require on an investment with a given beta.

Alpha

Alpha (α) is the ultimate goal for investors who seek to outperform the market on a risk-adjusted basis. Alpha is excess return, defined as

α = β Rm – Ri

where Ri is the return on a security i, Rm is return on the market, and β is beta.

Alpha represents the component of investment return due to selection and/or timing skill of an investor. Studies have found that in any given year, 75% of actively managed portfolios underperform passive market indices. Other evidence suggests that, after fees and expenses, only 5% of portfolio returns can be accounted for by alpha. Therefore, it is a rare investor who can consistently outperform a passive index on a risk-adjusted basis.