Overview

RioCan is one of Canada’s largest REITs, with a market cap of $13.9B (all dollars are Canadian). It manages, owns and develops 294 retail and mixed-use properties throughout Canada containing 45.149M square feet of net leasable area. Retail properties include urban retail, new format retail, and grocery- and non-grocery-anchored centers. As of the end of Q3 2017, RioCan had 6,415 tenancies, with total committed occupancy of 96.8 percent.

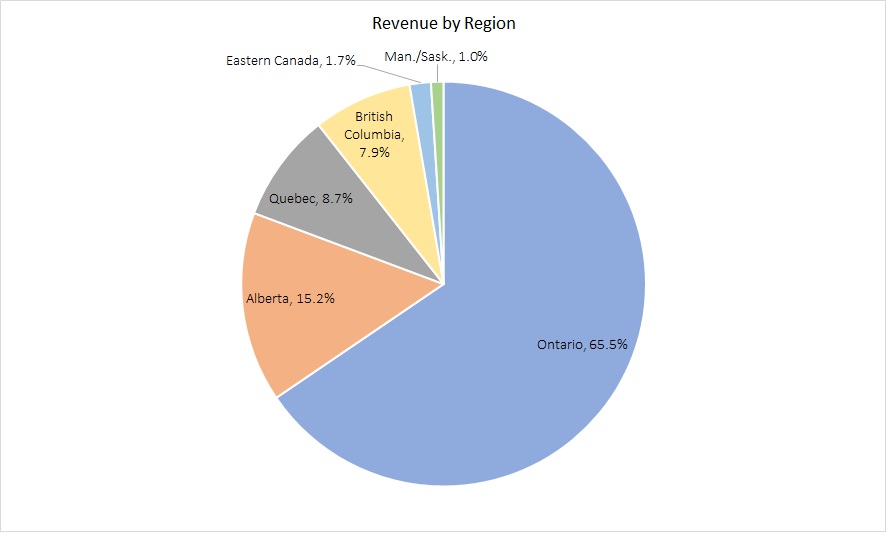

Rental revenue by region is as follows:

Recent Company Trends

RioCan is revamping its focus and will concentrate on six major Canadian markets: Toronto, Ottawa, Calgary, Edmonton, Vancouver and Montreal. To accomplish this, the company is selling off about 100 properties in other markets, worth more than $2B. These properties don’t meet RioCan’s growth targets. About half of the $1.5B in net proceeds will be used to raise exposure to the six markets from 75 percent to more than 90 percent, with more than half centered in greater Toronto. The strategy behind the shift is to concentrate on areas of strong population growth and demographic profile. More investment will go into mixed-use properties in prime, transit-oriented, high-density areas that attract Canadians to live, work and shop.

RioCan will use about half of the $1.5B sale net proceeds to protect and grow funds from operations (FFO), which is earnings plus depreciation and amortization minus gains on sales. It will accomplish this through unit (share) buybacks, development completions and organic growth. Elements of RioCan’s updated strategy also include:

- Investing $300M to $400M annually in the development pipeline within the six major markets

- Suspending its dividend reinvestment plan in order to concentrate on unit buybacks

- Intensifying the focus on developing residential, transit-oriented projects that will enhance the value of existing holdings

- Conservatively managing its balance sheet to ensure access to low-cost capital and liquidity.

Products

RioCan leases retail and office space and has recently begun a push into residential property. As of the end of 2017 Q3, RioCan is heavily concentrated in retail income-producing properties, which occupy almost 41M square feet, with another 0.83M under development. Office space totals 1.9M sq. ft., with 0.64M under development. All residential space, 0.79M sq. ft. is under development. Total combined occupancy is 96.8 percent. The percentage of rental revenue from anchor and national tenants is 84.4 percent, with the top four tenants in terms of annualized rental revenue being Loblaws/Shoppers Drug Mart, Canadian Tire Corporation, Walmart, and Cineplex/Galaxy Cinemas. Recent sales include six chartered bank branches in British Columbia. These properties were debt-free.

Financials

The six major Canadian markets account for 75.2 percent of annual rent revenue and net lettable area (NLA) of 68.7 percent, including 34.2 percent from Greater Toronto. Rental revenue for the first three quarters of 2017 was $851M compared to $818M in the same period of 2016. Property and asset management fees account for another $10.7M in revenue. Operating income for the period totaled $550M compared to $519M for 2016 same period. Net operating income for the period was 63.2 percent of rental revenue. Other income, from interest, joint ventures, fair value gains and other sources was $128M.

As of the end of 2017 Q3, RioCan had the following financial statistics:

| Current Ratio | 75% |

| Financial Leverage | 1.79% |

| Debt/Equity | 68% |

| Gross Margin | 63.3% |

| Return on Assets | 4.71% |

| Return on Equity | 8.46% |

| Interest Coverage | 4.91 |

| Revenue Growth | 1.50% |

| Operating Income Growth | 3.86% |

| Earnings per Share Growth | -25.33% |

| Earnings per Share | $2.03 |

| Dividend | $1.41 |

| Payout Ratio | 68.8% |

| Free Cash Flow | $49M |

| Free Cash Flow/Sales | 4.25% |

| Free Cash Flow/Net Income | 0.07% |

| FFO Growth | 7.9% |

| FFO/Share Growth | 7.5% |

| Same Property NOI Growth | 2.4% |

At the end of 2017, RioCan had the following statistics:

| Price/Share | $24.69 |

| Price/Cash Flow | 22.0 |

| Price/Book | 1.0 |

| Price/Sales | 7.0 |

| Price/Earnings | 12.0 |

| Dividend Yield | 5.71% |

| Market Cap | $8.1B |

Outlook

RioCan’s Q3 report showed an improving occupancy ratio and growing FFO. It has so far withstood the challenge posed by the growing competition from e-commerce, with improved operating and financial results in almost all categories. One reason for its higher occupancy ratio was new leasing to former Target stores in RioCan’s portfolio, which required considerable redevelopment costs. This upbeat occupancy story will suffer slightly from the liquidation of Sear’s Canadian stores, which currently rented a total of 381,000 square feet at nine locations. However, the revenue impact is expected to be only -0.6 percent. The decrease in weighted average interest rate bodes well for future cost of capital.

The biggest factor affecting the REIT’s outlook is its growth plan for the six major Canadian markets, including the heavy concentration in Greater Toronto. New immigrants to Canada overwhelmingly reside in the top three urban area. RioCan’s investments in transit facilities will help grow the value and rental income of nearby properties. The company is strategically redeveloping retail properties and developing new residential and office spaces, as well as some vacant properties. By concentrating on densely populated areas should yield higher rents and sales. Diversification will help reduce exposure to the retail sector.

With an attractive share valuation and historically low Price to Adjusted FFO ratio, RioCan looks like a solid bet in the Canadian REIT space over the intermediate term for capital appreciation and yield.

Sources

http://s1.q4cdn.com/847730316/files/documents_financial/2017/Q3/Q3-2017-Interim-Report.pdf

https://www.reuters.com/finance/stocks/financial-highlights/REI_u.TO

https://seekingalpha.com/article/4125241-high-quality-reit-performing-well-strong-outlook