Overview

Dream Office REIT leases and manages high-quality office properties primarily in the Toronto real estate market. Formerly known as Dundee REIT, Dream Office owns 46 properties with 8.5M square feet of gross leasable space. The average tenant leases 11,000 square feet and has 4.7 years left on its lease term. Dream Office has about 800 employees, $14B in assets and a 90.3 percent portfolio occupancy rate. The REIT’s objectives are to improve risk-adjusted returns, improve the quality of its portfolio holding and improve its balance sheet.

Recent Company Trends

Dream Office has recently completed a two-year divestiture program that shed properties worth $3.2 billion. Most of the selloff was focused on Alberta properties that had previously been purchased in the early part of the decade in an attempt to diversify beyond the Toronto region. The foray in Calgary was ill-timed, as it coincided with an economic turndown in Canada related to the energy markets. Several Toronto properties that were not amenable to redevelopment were sold in 2017. The REIT’s new focus is to redevelopment and intensification (expansion at existing high-density sites) in downtown Toronto. Some of the proceeds from the divestiture program have been used to buy back REIT shares. As of the end of 2017 Q3, Dream Office has repurchased 33.9M REIT shares and cut its dividend from $2.24 per share to $1.00.

The REIT’s strategic plan is now focused on three primary goals:

- Repaying debt: Over the last two years, Dream Office reduced its net debt/gross book value ration from 48.3 percent to 39.5 percent.

- Share buyback: The number of outstanding shares has dropped from 113M to 81M.

- Reinvesting in current holdings: Assets under development consideration went from zero to six since the end of 2015.

Holdings

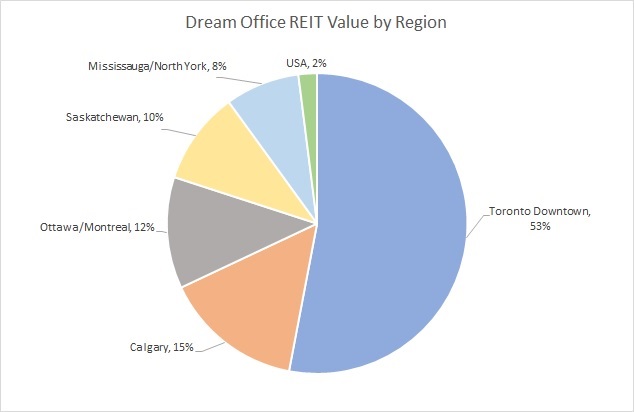

Dream office currently has 46 properties in eight markets, with a total value of $2.9B. The geographic distribution of property values is shown in the following chart:

The REIT’s top 10 tenants by gross rental revenue are:

- Government of Canada

- Government of Ontario

- State Street Trust Company

- Newalta Corporation

- Bell Canada

- International Financial Data Services

- Cenovus Energy

- Government of Saskatchewan

- Government of Quebec

- AON Canada Inc.

In all, Dream Office has 774 tenants that include Canada’s major law firms and banks, as well as many small- to medium-sized businesses.

The decision by Dream Office to concentrate its portfolio in the Greater Toronto Area (GTA) is based on the following factors:

- Toronto is the home to about 40 percent of the country’s business headquarters

- About one-quarter of Canada’s population lives in the GTA

- The workforce is highly education

- Toronto is one of North America’s fastest growing cities

- Toronto Downtown has the lowest vacancy rate in North America, with a 97.7 percent in-place and committed occupancy, with a weighted average lease term of 5.2 years

- Close proximity fo public transportation

Financials

For the nine months ending September 30, 2017, net rental income was $216.2M (compared to $306.5M year-over-year). Net income was $34.1M vs $-779.0M. The average lease term increased to 5.8 years from 4.8 years YOY.

For the trailing 12 months as of the end of 2017 Q3, Dream Office REIT had the following financial statistics:

| Current Ratio | 0.98 |

| Financial Leverage | 2.08 |

| Debt/Equity | 0.72 |

| Gross Margin | 55.2% |

| Return on Assets | -1.44% |

| Return on Equity | -3.10% |

| Interest Coverage | 0.39 |

| Revenue Growth | -102.8% |

| Operating Income Growth | -37.07% |

| Earnings per Share | $-0.85 |

| Dividend per Share | $1.25 |

| Payout Ratio | - |

| Free Cash Flow | $71M |

| Free Cash Flow/Sales | 12.74% |

| Free Cash Flow/Net Income | -1.07 |

As of February 9, 2018, Dream Office REIT had the following statistics:

| Price/Share | $17.06 |

| Price/Cash Flow | 16.5% |

| Price/Book | 1.18% |

| Forward Price/Earnings | 38.96 |

| Dividend Yield | 5.47% |

| Market Cap | $1.59B |

Outlook

Dream Office share prices rose to about 19% since its low of $13.82 in March 2017. This reflects growing optimism now that Dream Office has completed its write-down and divestiture plan and is concentrating on the Toronto office market. The company’s current focus is on redeveloping its current core properties. The strategy appears to be a good one, although it lacks diversification that is provided by other Canadian REITs.

Nevertheless, the company’s balance sheet is much improved. The debt-to-book-value ratio has fallen, and the company has more than $600M in available liquidity. Its face rate of interest is 3.93 percent and it has about $300M in unencumbered assets. Portfolio leasing momentum is rising. Dividends have been reduced in favor of aggressive share buybacks and intensification/redevelopment of existing properties. The biggest worry going forward is rising interest rates, which could dampen enthusiasm for Toronto office space in 2018.

Summary

Dream Office REIT is in a turnaround that appears to be working. It has streamlined its portfolio and is taking steps to increase the value of its existing holdings. For those who expect interest rates to remain low in the upcoming year, Dream Office is a viable investment on price dips, as its Forward P/E of almost 39 is on the high side.